Table of Content

Today a couple of important mortgage rates sank, though rates remain high compared to earlier this year. If you're in the market for a home loan, see how your payments might be affected by inflation. When rates go up, ARM borrowers can expect to pay higher monthly mortgage payments. This is a percentage added to the index rate by the lender to calculate your full interest rate. Sometimes lenders won’t add it on until the introductory, fixed-rate period ends, while others will include it from the start. Annual Percentage Rate represents the true yearly cost of your loan, including any fees or costs in addition to the actual interest you pay to the lender.

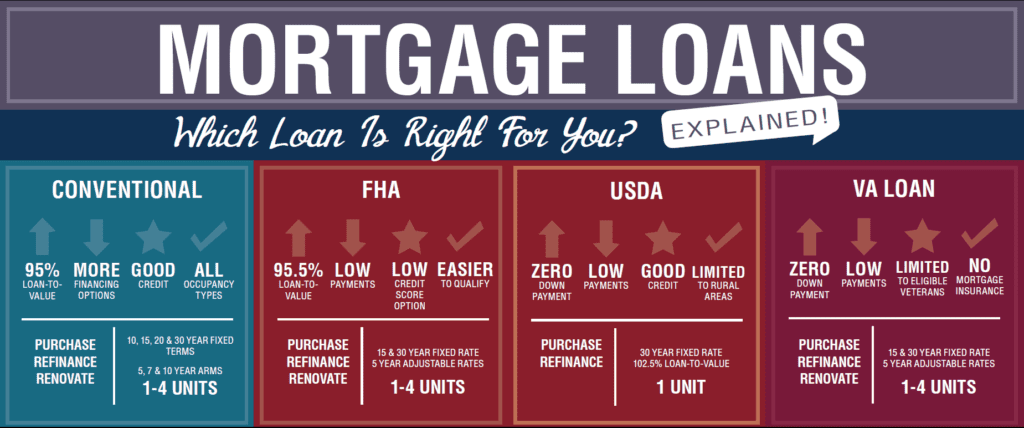

We offer several programs designed to help make homeownership more affordable. When getting a mortgage, be sure you understand what those rates really mean. Another key characteristic of ARMs is whether they are conforming or nonconforming loans. Conforming loans are those that meet the standards of government-sponsored enterprises like Fannie Mae and Freddie Mac.

Annual percentage yield (APR)

ARMs are also called variable-rate mortgages or floating mortgages. The interest rate for ARMs is reset based on a benchmark or index, plus an additional spread called an ARM margin. The typical index that is used in ARMs has been the London Interbank Offered Rate .

Conventional adjustable-rate mortgage loans typically feature lower interest rates and Annual Percentage Rates during the initial rate period than comparable fixed-rate mortgages. Yes, their favorable introductory rates are appealing, and an ARM could help you to get a larger loan for a home. However, it’s hard to budget when payments can fluctuate wildly, and you could end up in big financial trouble if interest rates spike, particularly if there are no caps in place. Doing this could allow you to make more affordable mortgage payments until you're ready to move. An adjustable-rate mortgage is a type of loan that carries an interest rate that is constant at first but changes over time. For the first few years, you'll typically pay a low fixed interest rate.

When you need a lower rate than what the market is offering.

When you’re stretching to buy your dream home, you want the lowest interest rate you can find. An adjustable-rate mortgage offers a potential solution—but there are risks if you plan to stay in your home long term. Adjustable-rate mortgages start off with a fixed interest rate, then float. 5The index (for 10/10 product) is the weekly average of the 10-year US Treasury securities adjusted to constant maturity of ten years, as made available by the Federal Reserve. The caps are 3% every adjustment and 6% lifetime based on the initial rate. 4The index (for 5/5 product) is the weekly average of the 5-year US Treasury securities adjusted to constant maturity of five years, as made available by the Federal Reserve.

They are packaged and sold off on the secondary market to investors. Nonconforming loans, on the other hand, aren't up to the standards of these entities and aren't sold as investments. Our mortgage team works with you to ensure that you get the options tailored to meet your needs. To prevent the interest rate from reaching too high over the life of the loan. A maximum increase which prevents any single change from being above an agreed upon percentage.

Lifetime cap

The APR may be increased after the closing date for adjustable-rate mortgage loans. ARMs may offer you flexibility but they don't provide you with any predictability as fixed-rate loans do. Borrowers with fixed-rate loans know what their payments will be throughout the life of the loan because the interest rate never changes. But because the rate changes with ARMs, you'll have to keep juggling your budget with every rate change. Although the rate of interest is fixed, the total amount of interest you’ll pay depends on the mortgage term. Traditional lending institutions offer fixed-rate mortgages for a variety of terms, the most common of which are 30, 20, and 15 years.

Our residential loan officers can help you decide which mortgage is right for your unique personal situation. Borrowers can plan for rate increases because they will be scheduled into the mortgage, but the amount of the increase is subject to market fluctuations. This means the borrower might refinance the property to a fixed-rate mortgage before the interest rate is scheduled to adjust. If you do decide to refinance your adjustable-rate mortgage to get a lower interest rate, you could be hit with a prepayment penalty, also known as an early payoff penalty.

What is an Adjustable Rate Mortgage or ARM Loan?

With consistent principal and interest payments, you could manage your money with more certainty. When you are ready to apply for a loan, you can reach out to a local mortgage broker or search online. Make sure to think about your current financial situation and your goals when trying to find a mortgage. But, Wood warns, you have to be prepared for your monthly payment to go up eventually. Workers in industries with little income-growth potential, like teachers or government employees, should probably steer clear. 1Lock and Shop program is available for 1st mortgage Jumbo loan purchase transactions only.

That’s how we’re able to offer great loans—and great rates—that our competitors can’t match. With an ARM, you have the option to refinance to a fixed-rate mortgage. It’s impossible to know what direction mortgage rates will go from day to day. That’s why a mortgage rate lock is such a useful tool because it protects you if rates go up. And with interest rates being relatively low right now, you should lock in your rate as soon as you can.

One of the major cons of ARMs is that the interest rate will change. This means that if market conditions lead to a rate hike, you'll end up spending more on your monthly mortgage payment. Hybrid ARMs offer a mix of a fixed- and adjustable-rate period. With this type of loan, the interest rate will be fixed at the beginning and then begin to float at a predetermined time.

We also saw a rise in the average rate of 5/1 adjustable-rate mortgages . You can pay off the principal amount faster than with a 30-year loan. Keep in mind that fifteen-year mortgages do have higher monthly payments. The average interest rates for both 15-year fixed and 30-year fixed mortgages were slashed.

The interest rate then may change each year thereafter once the initial fixed period ends. For example, with a 5/1 ARM loan for a 30-year term, your interest rate would be fixed for the initial 5 years and could fluctuate up or down each subsequent year for the next 25 years. One of the major benefits of an adjustable-rate loan is the introductory rate is usually lower than a traditional fixed-rate mortgage. This means the ARM loan can allow the borrower to buy more house with the same down payment than they could with a fixed-rate mortgage. With fixed-rate mortgages, you're locked into the same interest rate for the entire life of the loan, which is usually 15 or 30 years.

She has been in the accounting, audit, and tax profession for more than 13 years, working with individuals and a variety of companies in the health care, banking, and accounting industries. Please enter your home zip code so we can provide accurate information and personalized service. Buying a home is an important milestone and one of the biggest financial decisions you’ll make. Also, if you opt out of online behavioral advertising, you may still see ads when you log in to your account, for example through Online Banking or MyMerrill.

No comments:

Post a Comment